Reporting mechanisms

Caroline Burns Ph.D

Learning Objectives

At the end of this module, you will be able to

- Distinguish between required and voluntary governance disclosures.

- Evaluate the ethical and political tensions in ESG reporting.

- Explain how transparency shapes accountability in governance.

Required Governance Disclosures

Certain reporting mechanisms are mandated by law, especially for publicly listed firms. The U.S. Securities and Exchange Commission (SEC) requires companies to submit regular filings such as Form 10-K (annual report) and Form 10-Q (quarterly report), which disclose financial performance, risk factors, governance structures, and internal controls. Firms must detail their board composition, executive compensation, and any material changes in corporate governance.

On March 6, 2024, the SEC adopted new rules that require certain large firms to disclose climate-related risks in their standard filings, focusing on material risks and governance practices. [see the Press Release below]. The rules do not mandate Scope 3 emissions reporting and are currently stayed due to legal challenge. This means their implementation has been temporarily paused while legal challenges are resolved.

In addition to SEC rules, stock exchanges like the New York Stock Exchange (NYSE) and NASDAQ impose requirements that include specific governance practices. These often include requirements for audit committees, codes of ethics, and board independence. Although not always framed as ethical reporting, the disclosures reinforce transparency, fiduciary responsibility, and accountability to shareholders.

SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors

For Immediate Release

2024-31

Washington D.C., March 6, 2024 —

The Securities and Exchange Commission today adopted rules to enhance and standardize climate-related disclosures by public companies and in public offerings. The final rules reflect the Commission’s efforts to respond to investors’ demand for more consistent, comparable, and reliable information about the financial effects of climate-related risks on a registrant’s operations and how it manages those risks while balancing concerns about mitigating the associated costs of the rules.

“Our federal securities laws lay out a basic bargain. Investors get to decide which risks they want to take so long as companies raising money from the public make what President Franklin Roosevelt called ‘complete and truthful disclosure,’” said SEC Chair Gary Gensler. “Over the last 90 years, the SEC has updated, from time to time, the disclosure requirements underlying that basic bargain and, when necessary, provided guidance with respect to those disclosure requirements.”

Chair Gensler added, “These final rules build on past requirements by mandating material climate risk disclosures by public companies and in public offerings. The rules will provide investors with consistent, comparable, and decision-useful information, and issuers with clear reporting requirements. Further, they will provide specificity on what companies must disclose, which will produce more useful information than what investors see today. They will also require that climate risk disclosures be included in a company’s SEC filings, such as annual reports and registration statements rather than on company websites, which will help make them more reliable.”

… Before adopting the final rules, the Commission considered more than 24,000 comment letters, including more than 4,500 unique letters, submitted in response to the rules’ proposing release issued in March 2022.

The adopting release is published on SEC.gov and will be published in the Federal Register. The final rules will become effective 60 days following publication of the adopting release in the Federal Register, and compliance dates for the rules will be phased in for all registrants, with the compliance date dependent on the registrant’s filer status.

Last Reviewed or Updated: March 6, 2024

Voluntary Governance Disclosures

Beyond these legal requirements, firms may choose to report out on a wider range of governance-related information. Voluntary disclosures have become a key means of communicating ethical commitments, stakeholder responsiveness, and long-term strategic thinking. These disclosures are neither required nor enforced by regulatory agencies but are a response to emerging and established industry norms, investor expectations, and public and civil society accountability demands.

Voluntary governance reporting often follows the pattern of ESG reporting: Environmental, Social, and Governance. ESG is not a formal regulation but a conceptual framework for grouping non-financial risks and performance used by investors, rating agencies, and civil society to assess how firms address their broader responsibilities to society and the natural world. The environmental component includes disclosures about emissions, energy use, and climate adaptation, the governance component includes ethical leadership, board oversight, whistleblower protections, and compliance procedures, and finally, the social component (which is often the least robust ) focuses on labor standards, diversity and inclusion, pay equity, supply chain ethics, and respect for human rights for example.

Firms that voluntarily report on ESG issues typically do so using one or more established frameworks. These include:

- GRI (Global Reporting Initiative) [New Tab]: Provides detailed standards for sustainability reporting, including metrics for labor rights, community impact, and anti-corruption. [see the Press Release below]

- SASB (Sustainability Accounting Standards Board) [New Tab] and ISSB (International Sustainability Standards Board) [New Tab]: Offer industry-specific metrics tied to financial materiality. ISSB was the culmination of the work of the Task Force on Climate-related Financial Disclosures (TCFD) [New Tab].

- UNGC (United Nations Global Compact) [New Tab]: Encourages firms to align with ten universal principles related to human rights, labor, environment, and anti-corruption.

- SDGs (Sustainable Development Goals) [New Tab]: Provide a global ethical benchmark that some companies use to structure their social and environmental goals.

RELEASE FROM GLOBAL REPORTING INTIATIVE

The global standards for sustainability impacts

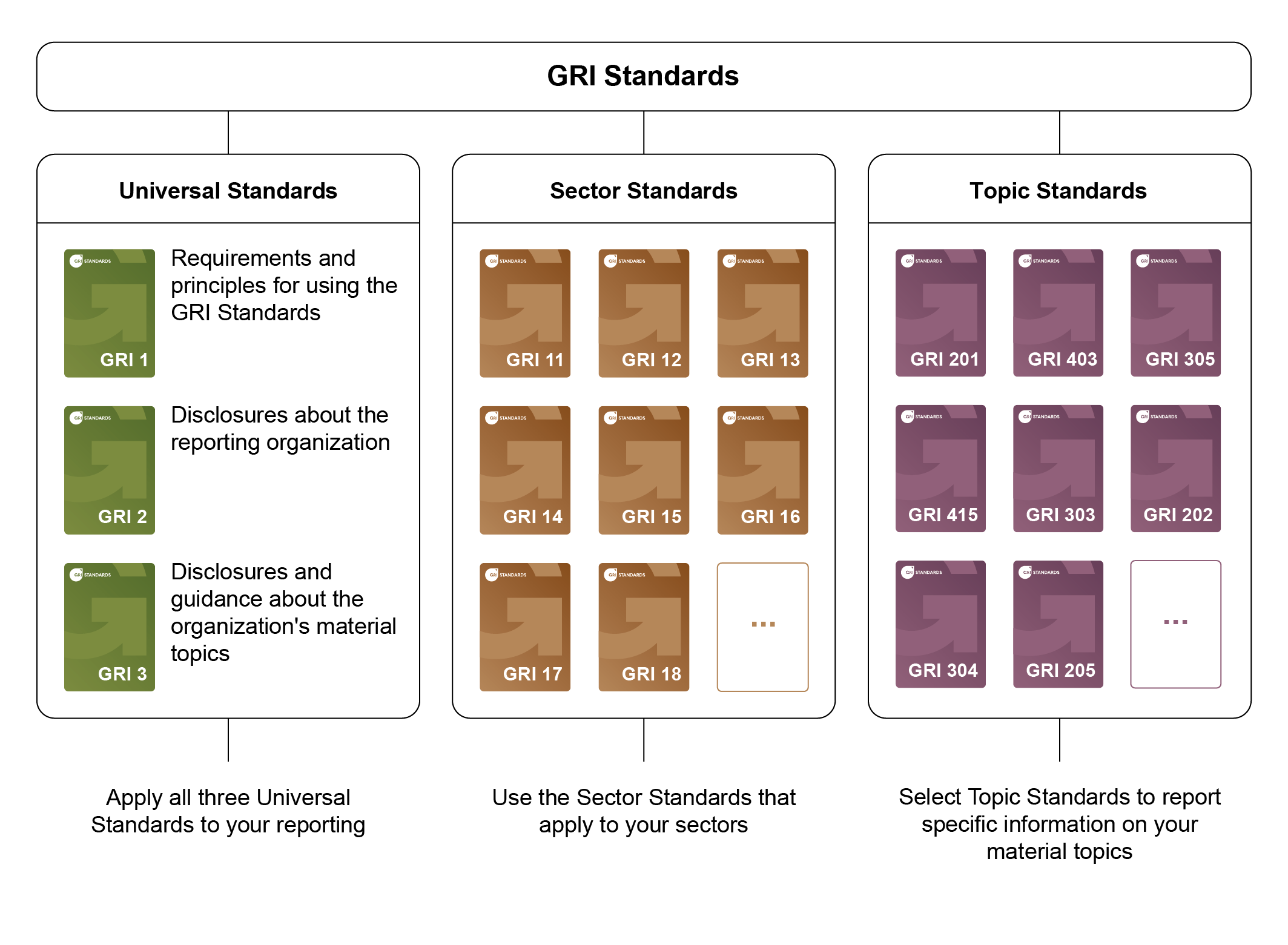

The GRI Standards enable any organization – large or small, private or public – to understand and report on their impacts on the economy, environment and people in a comparable and credible way, thereby increasing transparency on their contribution to sustainable development. In addition to companies, the Standards are highly relevant to many stakeholders – including investors, policymakers, capital markets, and civil society.

The Standards are designed as an easy-to-use modular set, delivering an inclusive picture of an organization’s material topics, their related impacts, and how they are managed.

- Universal Standards – incorporate reporting on human rights and environmental due diligence, in line with intergovernmental expectations, and apply to all organizations;

- Sector Standards enable more consistent reporting on sector-specific impacts;

- Topic Standards – list disclosures relevant to a particular topic.

These frameworks differ in orientation. GRI and the SDGs emphasize broader stakeholder concerns. SASB and ISSB target investor-relevant risks. Most firms combine elements from multiple frameworks to align with both social expectations and capital market norms.

For firms operating globally, especially in the European Union, ESG-related reporting is rapidly becoming mandatory. The Corporate Sustainability Reporting Directive (CSRD) [New Tab], adopted by the European Commission in 2022 and effective from 2024, requires firms operating in the EU, including certain non-EU companies with significant EU revenue, to provide detailed ESG disclosures under the European Sustainability Reporting Standards (ESRS) [New Tab] [see the Press Release below]. These standards use a double materiality approach; this means that firms must report both how sustainability issues affect them and how their operations affect people and the planet.

RELEASE FROM EUROPEAN COMMISSION

New rules on corporate sustainability reporting: The Corporate Sustainability Reporting Directive

On 5 January 2023, the Corporate Sustainability Reporting Directive (CSRD) entered into force. It modernises and strengthens the rules concerning the social and environmental information that companies have to report. A broader set of large companies, as well as listed SMEs, will now be required to report on sustainability. Some non-EU companies will also have to report if they generate over EUR 150 million on the EU market.

The new rules will ensure that investors and other stakeholders have access to the information they need to assess the impact of companies on people and the environment and for investors to assess financial risks and opportunities arising from climate change and other sustainability issues. Finally, reporting costs will be reduced for companies over the medium to long term by harmonising the information to be provided.

The first companies will have to apply the new rules for the first time in the 2024 financial year, for reports published in 2025.

Companies subject to the CSRD will have to report according to European Sustainability Reporting Standards (ESRS). The standards are developed in a draft form by the EFRAG, previously known as the European Financial Reporting Advisory Group, an independent body bringing together various different stakeholders.

The first set of ESRS was published in the Official Journal on 22 December 2023 under the form of a delegated regulation. These standards apply to companies under the scope of the CSRD regardless of which sector they operate it. They are tailored to EU policies, while building on and contributing to international standardisation initiatives.

The CSRD also requires assurance on the sustainability information that companies report and will provide for the digital taxonomy of sustainability information.

Recent developments in 2025 have proposed significant changes to the CSRD scope. The European Commission has proposed limiting CSRD requirements to only the largest companies (those with more than 1,000 employees), which would reduce the reporting burden on smaller companies while at the same time maintaining focus on organizations with the greatest environmental and social impact.

Challenges to Voluntary Reporting Efforts

Voluntary reporting is not without its challenges. Critics argue that ESG disclosures lack comparability and may distract from financial fundamentals. Others question whether firms use ESG to deflect scrutiny or advance reputational goals without real accountability. The social dimension, which includes diversity, labor rights, and community impact, is especially underdeveloped. Ethical commitments are difficult to reduce to metrics, and few standards require firms to disclose outcomes rather than intentions.

Political backlash in the U.S. has further complicated the ESG landscape. Some lawmakers and commentators argue that ESG reporting imposes ideological goals on business or violates fiduciary responsibilities. Others see such reporting as essential to risk management, public trust, and long-term value creation.

In sum, the governance disclosures a firm chooses to make, or not, serve as a window into its ethical priorities. Mandated reports satisfy minimum legal requirements. Voluntary disclosures reveal how a firm interprets its responsibilities beyond the law; it is an expression of what the firm stands for.

Watch this video from Morrison Foerster, an international law firm.

Video 6.2. ESG Backlash and Politicization by Morrison Foerster

Knowledge check

Companies whose shares are traded on public stock exchanges. These firms are subject to heightened disclosure requirements, including mandatory governance and financial reporting. See more

Official reports and disclosures that companies submit to regulatory bodies such as the SEC. These filings typically include financial statements, risk disclosures, governance details, and ESG reports, and are legally required for publicly traded firms.

Significant alterations in a company's operations, governance, or risk profile that could reasonably influence investor decisions. Public companies are legally required to disclose material changes in their filings.

Risks that are likely to have a meaningful impact on a firm's financial condition or performance. In ESG reporting, materiality refers to the relevance of sustainability issues to both investors and affected stakeholders.

Greenhouse gas emissions that occur in a company's value chain but are not directly owned or controlled by the company. This includes emissions from suppliers, product use, business travel, and waste disposal. Scope 3 is often the largest share of a company's total carbon footprint.

Government bodies tasked with enforcing laws and standards. In the U.S., examples include the SEC (financial reporting), EPA (environmental protection), and OSHA (workplace safety). Regulatory agencies define and oversee required corporate disclosures.

A broad term that refers to organizations and institutions outside of government and business, including NGOs, advocacy groups, professional associations, and grassroots movements. Civil society actors often influence corporate accountability and shape ESG expectations.

Organizations that assess and score the creditworthiness or ESG performance of firms. This includes credit agencies (Moody's, S&P) and ESG rating providers (MSCI, Sustainalytics). Their evaluations influence investor decisions and can shape corporate access to capital.

The executive branch of the European Union responsible for proposing legislation, enforcing EU laws, and managing day-to-day operations. It plays a central role in developing and enforcing sustainability and corporate reporting regulations such as the CSRD.

{kind=link}